Summary

Increasing credit risk and economic uncertainties require greater underwriting discipline. Structured financial statement analysis and balance sheet analysis enable lenders to make informed judgments about repayment ability with clarity and confidence. This guide offers a framework to improve credit analysis and portfolio stability.

Introduction

A single misunderstood ratio can quietly undermine an entire credit portfolio. In the current lending landscape, incomplete financial statement analysis can result in unnecessary defaults and late risk identification. Small holes in liquidity or leverage analysis can produce large losses in the long run.

Lenders are under growing regulatory, competitive, and borrower complexity pressures. It is no longer adequate to simply review reports. There is a need to interpret trends, confirm assumptions, and record conclusions. A systematic financial statement analysis guide for lenders helps to ensure clarity, consistency, and defensibility of credit decisions.

In this blog, we will examine how lenders can leverage disciplined financial statement analysis, improve sheet analysis, assess borrower stability through ratio analysis, and incorporate systematic governance into lending processes.

| “Financial statements are a window into management’s decisions and a company’s reality.”

— Mary Buffett |

What Is Financial Statement Analysis?

Financial statement analysis is the structured evaluation of a borrower’s financial reports to determine creditworthiness and repayment capacity. It enables lenders to extract clear, measurable insights about a borrower’s overall financial health.

Through standardized analysis, lenders systematically assess profitability, liquidity, leverage, and operational efficiency. This structured approach ensures that credit decisions are based on objective financial indicators rather than subjective judgment. Without consistency, loan evaluations can become fragmented, increasing the risk of inaccurate or biased decisions. A financial statement analysis guide for lenders helps lenders improve documentation, enhance transparency, and facilitate regulatory compliance.

| Did you know? |

|---|

| About 82% of small businesses fail because of poor cash flow management, showing how critical financial analysis and liquidity evaluation are for sustainable growth. |

Understanding Core Reports: Balance Sheet Analysis and Income Statement Review

Underwriting starts with two essential documents. The income statement provides information about the business’s performance in terms of revenue generation and cost of operation. Balance sheet analysis provides information about the financial position of the business at a given time.

The income statement provides information to the lender about the sustainability of the business’s earnings and cost management. The sheet analysis provides information to the lender about the liquidity position of the business and its susceptibility to debt. A business can be making increasing profits while having too much short-term debt. Reviewing both statements together ensures a holistic view of financial health. Trend comparison across multiple years strengthens insight and reduces reliance on isolated performance periods.

How Lenders Use It

Lenders use financial statement analysis to make informed credit decisions and manage risk effectively.

- Credit Approval: Assess repayment capacity before sanctioning loans.

- Risk Detection: Identify early warning signs like weak cash flow or rising debt.

- Loan Structuring: Set appropriate terms based on financial strength.

- Portfolio Monitoring: Track borrower performance post-disbursement.

It transforms lending from judgment-based decisions to structured, data-driven evaluation.

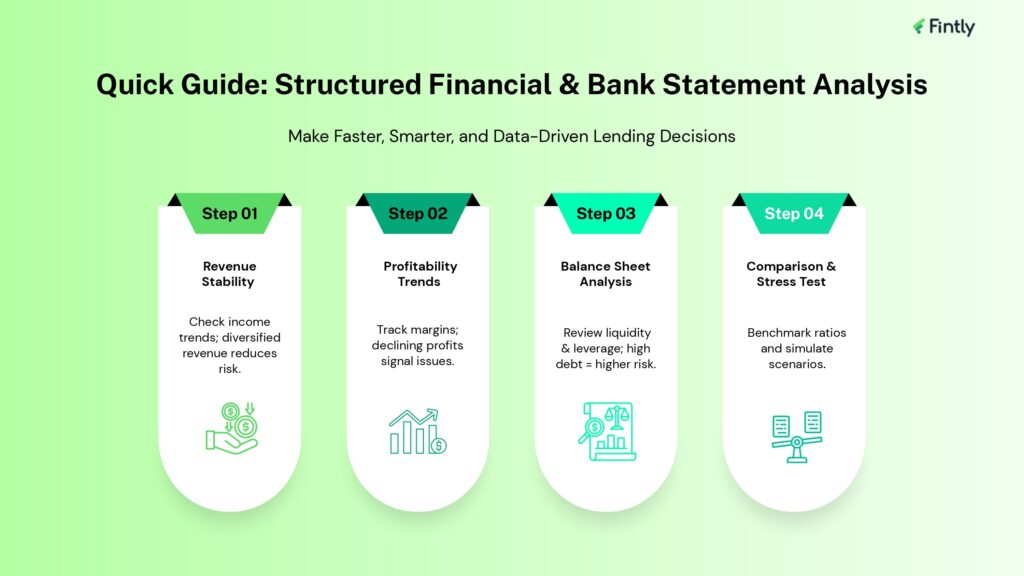

Step-by-Step Financial Statement Analysis Guide for Lenders

A good financial statement analysis guide for lenders involves a systematic approach. This makes the analysis less subjective and more comparable among borrowers.

Step 1: Revenue Stability Analysis

Analyze the revenue trends and customer base from the income statement. Diversified revenue streams make the business less dependent.

Step 2: Profitability Trend Analysis

Analyze gross and net profit margins. A steady decline indicates inefficient operations or market pressure.

Step 3: Balance Sheet Analysis

Analyze liquidity ratios, working capital, and leverage ratios systematically. A high short-term debt burden makes repayment difficult.

Step 4: Comparison and Stress Test

Compare financial ratios to industry peers and test for adverse outcomes.

Together, bank statement analysis provide a systematic method that enables lenders to make credit decisions quickly, systematically, and justifiably, transforming lending into a structured, data-driven process.

Key Ratios That Enhance Financial Insight

Ratios simplify financial information into meaningful indicators. Ratios enhance financial statement analysis by allowing objective comparison and timely risk identification. Financial institutions that utilize ratio analysis in lending are more resilient in their portfolios.

| Category | Ratio | Purpose |

| Liquidity | Current Ratio | Short-term repayment ability |

| Leverage | Debt-to-Equity Ratio | Financial risk exposure |

| Profitability | Net Profit Margin | Operational efficiency |

| Coverage | Interest Coverage Ratio | Debt servicing strength |

| Efficiency | Asset Turnover Ratio | Asset utilization effectiveness |

These ratios complement structured balance sheet analysis and performance trend evaluation. Numbers must be interpreted within industry context and management capability assessment.

Identifying Red Flags Before They Escalate

Early risk identification ensures the stability of the portfolio. In-depth analysis of financial statement analysis can identify risk indicators like sudden surges in receivables, deteriorating working capital, or unstable revenue trends. A financial statement showing profit growth accompanied by poor operating cash flow performance could indicate accounting treatment rather than genuine trends.

Similarly, balance sheet analysis can identify trends of rising dependence on short-term borrowings or deteriorating equity reserves. Such trends are early warning signs of potential liquidity problems. Early and systematic risk analysis can help lenders protect themselves against risks.

| Did you know? |

|---|

| Companies that monitor financial ratios regularly are up to 3x more likely to spot early warning signs of distress, improving risk management outcomes. |

Financial Statement Analysis in Volatile Economic Conditions

Borrower risk is amplified by macroeconomic uncertainty. Inflation, supply chain issues, and rising interest rates have a direct impact on profitability and liquidity. Effective financial statement analysis needs to go beyond the historical analysis process and incorporate assumptions about future performance.

Stress testing for various scenarios can improve resilience. Analyze the impact of revenue decline on debt service coverage ratios. Test liquidity on delayed receivables. A structured financial statement analysis guide for lenders incorporates these stress tests into the normal lending process. Institutions that use forward-looking analysis frameworks have reduced credit volatility in times of crisis.

Supporting Intelligent Credit Infrastructure

Contemporary lending entities demand smart infrastructure that support structured assessment. Fintly provides AI-driven credit infrastructure that aims to optimize the underwriting process and increase transparency.

Financial statement analysis integrated into digital processes enables lenders to process statements faster and more consistently. The automated bank statement analysis increases accuracy and remains audit ready. Entities adopting smart infrastructure are poised for growth.

Leveraging Technology for Structured Evaluation

Digital transformation is also changing the way credits are processed. Technology is now used to improve financial statement analysis by extracting and normalizing data quickly.

Automated balance sheet analysis improves ratio analysis quality and consistency. Automated income data processing ensures consistency in borrower analysis. Although automation increases efficiency, human expertise is still essential. Integrating intelligent analytics with human expertise ensures scalable and managed lending growth.

Why Fintly Is a Trusted Leader in Intelligent Credit Decisioning

At Fintly, we leverage the power of analytics, automation, and domain knowledge to revolutionize the way lenders assess financial information. Our smart credit solutions help lenders simplify financial statement analysis, improve risk insights, and hasten underwriting processes without sacrificing accuracy.

With the backing of progressive financial institutions, Fintly enables lenders to transition from traditional assessments to systematic, scalable, and data-driven decision-making – helping them build better portfolios with confidence and control.

Turning Financial Analysis into Confident Lending Decisions

Structured financial statement analysis enables lenders to convert financial statements into strategic credit information. When lenders use a financial analysis guide, they are able to gain better insight into the creditworthiness of borrowers.

Structured sheet analysis, in addition to analyzing profitability and cash flow, helps lenders reduce uncertainty and increase the resilience of their portfolios.

Structured financial statement analysis helps lenders make informed lending decisions. Institutions that emphasize disciplined evaluation frameworks are able to build better portfolios and grow sustainably. Ready to strengthen your underwriting process? Book a demo with Fintly and see how intelligent financial analysis can power faster, smarter, and more confident credit decisions.

| Key Takeaways |

|---|

|

Author

Subject Matter Experts (Lending) Fintly.co

Vijay Mali is a results-driven professional with deep expertise in HFC/NBFC startups, compliance, and underwriting. He specializes in delivering end-to-end solutions for financial institutions, focusing on Business Rule Engines (BRE), workflow automation, and AI-driven credit decision-making. He is passionate about leveraging Machine Learning (ML) scorecards and AI-powered risk assessment to optimize lending processes and drive digital transformation in the financial sector.