Summary

This blog establishes Unified Financial Intelligence as the cornerstone of future lending by showcasing its role in enabling AI-driven lending solutions, holistic underwriting, and data-driven decision making. By emphasizing data-driven lending models for smarter and more inclusive loan approvals and AI-driven credit decisioning using alternative data for better underwriting, this approach transforms credit risk management and expands financial inclusion effectively.

Introduction

The lending landscape is changing significantly with the rise of Unified Financial Intelligence. By bringing together different financial data streams and using analytics, this approach is changing how lenders evaluate risk, approve loans, and assist customers.

Traditional credit scoring methods often fail to meet the demands of today’s complex financial environment. AI-powered lending solutions that leverage alternative data have become essential for reaching underserved markets and enabling faster, more informed decision-making. AI-driven capabilities of Fintly help lenders move beyond legacy credit models to assess real-world financial behavior with greater accuracy.

Millions of individuals and small businesses are still left out of traditional credit systems. By implementing holistic underwriting and data-driven decision-making, financial institutions can create new chances for smart credit decisions, promoting financial inclusion on a larger scale.

This blog looks at how Unified Financial Intelligence combines various data points to give a complete financial picture. This allows for smarter and more inclusive loan approvals.

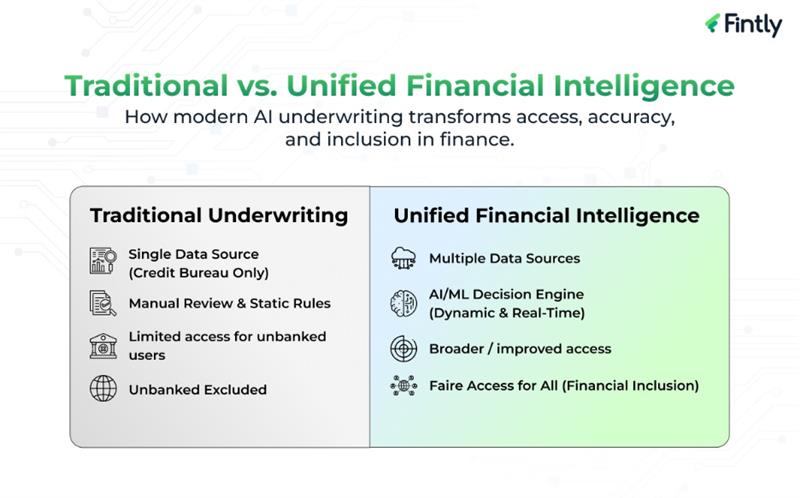

The Limits of Traditional Lending

Traditional lending models are like trying to navigate a complex landscape with an outdated map. They provide a basic outline but miss the rich details needed for a successful journey. This system suffers from three critical flaws:

- The Thin-File Problem: According to the World Bank, nearly 1.7 billion adults remain “unbanked,” with no credit history at all. Traditional systems have no way to assess them.

- A Rear-View Mirror Approach: Credit scores look backward, not forward. They cannot capture a borrower’s current financial stability or future potential.

- Data Silos: Banking, utility, rental, and transaction data live in separate silos. Lenders make decisions with only a fraction of the available information.

The result? Missed opportunities for lenders and frustrating, often unfair, experiences for borrowers.

| INSIGHT : The True Cost of Outdated Credit Systems |

|---|

| According to industry and regulatory estimates, approximately 40–50 million Americans are either credit invisible or have insufficient credit history. This represents a substantial underserved segment of the U.S. lending market, which is estimated to be worth several hundred billion dollars annually. Reliance on traditional credit scoring models limits access for these consumers and constrains potential growth opportunities for financial institutions. |

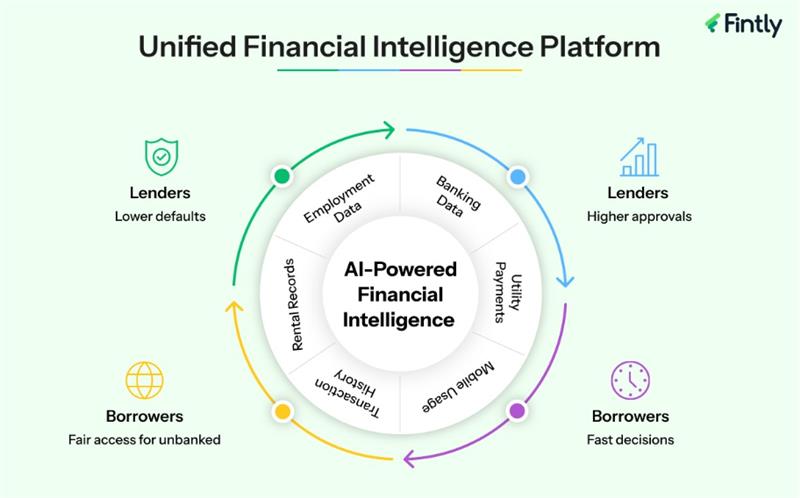

What is Unified Financial Intelligence?

Unified Financial Intelligence refers to the consolidation of diverse financial data sources and intelligent analytics into a single, cohesive framework to enhance credit decision-making. It goes beyond traditional methods by combining:

- Alternative data in lending such as mobile usage, utility payments, and transaction history

- AI-driven lending solutions to analyze and predict creditworthiness

- Data-driven decision making that factors in behavioral and contextual insights

- Holistic underwriting that evaluates borrowers comprehensively rather than focusing on limited credit history

This intelligence allows lenders to craft personalized loan offers quickly and with higher accuracy. Through Unified Lending Interfaces (ULI) , financial institutions can seamlessly access, and share verified data in real time, drastically reducing loan processing times and boosting customer experience.

The Role of AI-Driven Credit Decisioning in Lending

Artificial intelligence (AI) is at the heart of Unified Financial Intelligence. AI-driven credit decisioning using alternative data for better underwriting enables lenders to:

- Analyze vast amounts of structured and unstructured data

- Detect patterns and anomalies that humans might overlook

- Provide dynamic risk scores that adapt to market changes

Industry research, including insights from McKinsey, indicates that lenders adopting AI-powered underwriting can improve loan approval efficiency, enhance risk assessment, and reduce credit losses. These improvements help financial institutions unlock new revenue opportunities while managing risk more effectively.

| Ready to Transform Your Lending Operations? |

|---|

| Is your institution missing out on creditworthy borrowers? See how Unified Financial Intelligence can help you: |

| ✓ Reduce default rates |

| ✓ Increase loan approvals |

| ✓ Reach broader consumer market |

| ✓ Speed up loan processing with AI automation |

| [Book a Free Demo] → Discover next-generation lending |

Did you know?

AI-powered underwriting can significantly reduce loan processing time, from days to minutes in many use cases by rapidly analyzing large volumes of structured and alternative data in real time.

Advantages of Holistic Underwriting and Smart Credit Decisioning

Traditional underwriting relies heavily on credit scores and limited financial data, often excluding large segments of the population. In contrast, holistic underwriting evaluates a borrower’s entire financial behavior and context, including cash flow, transaction trends, and alternative credit data. This approach enables:

- More accurate assessment of credit risk for thin-file or no-file borrowers

- Greater inclusion of underserved populations, promoting financial inclusion

- Enhanced fraud detection and compliance adherence

Additionally, smart credit decisioning leverages machine learning models to continuously learn from new data, ensuring updates in borrower risk profiles are timely and precise.

Data-Driven Lending Models for Smarter and More Inclusive Loan Approvals

One of the most promising developments powered by Unified Financial Intelligence is the rise of data-driven lending models for smarter and more inclusive loan approvals. These models integrate diverse data points:

- Traditional financial histories

- Alternative data like mobile usage and utility payments

- Behavioral data from digital transactions

By incorporating this wide array of information, lenders make decisions that balance risk with greater inclusivity.

| INSIGHT : From Exclusion to Inclusion Through Data |

|---|

| The shift to Unified Financial Intelligence represents a fundamental reimagining of creditworthiness. Traditional systems ask, “What is your credit score?” Unified intelligence asks, “What is your financial story?” A gig worker with inconsistent income but steady cash flow management, or a recent immigrant with no U.S. credit history but reliable bill payments, can all demonstrate creditworthiness through alternative data. This holistic view does not lower standards; it broadens the lens through which lenders evaluate risk. |

The Tangible Benefits: A Win-Win for Lenders and Borrowers

The impact of this shift is profound and mutually beneficial.

For Lenders:

- Sharper Risk Management: Reduce default rates by identifying subtle risk factors and fraud patterns across unified data.

- Increased Portfolio Growth: Tap into lucrative, underserved markets like freelancers, gig workers, and small businesses.

- Operational Efficiency: Automate underwriting tasks, allowing human agents to focus on complex cases.

For Borrowers:

- Fairer Access to Capital: Your financial story is heard in its entirety, not just one chapter.

- Personalized Products: Receive loan offers with terms, rates, and amounts tailored to your unique financial situation.

- A Frictionless Experience: Enjoy a digital, fast, and transparent application process.

How Different Sectors Benefit from Unified Financial Intelligence

The transformation enabled by Unified Financial Intelligence extends across various lending segments, each experiencing unique advantages:

Consumer Lending and Personal Finance

Traditional consumer lending often relies on FICO scores that may not reflect current financial health. Unified Financial Intelligence analyzes real-time transaction data, income stability, and spending patterns to provide a current financial snapshot. This approach particularly benefits younger borrowers from building credit, enabling them to access personal loans, credit cards, and auto financing based on demonstrated financial responsibility rather than limited credit history.

Small Business and Commercial Lending

Small businesses frequently struggle to secure financing due to thin business credit files or seasonal revenue fluctuations. By incorporating alternative data such as payment processing volumes, inventory turnover, and accounts receivable patterns, lenders gain visibility into actual business performance. AI-driven lending solutions can distinguish between businesses with temporary cash flow challenges and those with structural problems, enabling more nuanced risk assessment.

Microfinance and Emerging Market Lending

In developing economies where traditional credit infrastructure is limited, Unified Financial Intelligence becomes transformative. Mobile money transaction history, utility payment records, and community lending patterns provide rich data for credit assessment. Lenders can serve previously invisible populations, expand financial inclusion while maintain responsible lending standards. This approach has proven particularly effective in regions with high mobile penetration but limited banking infrastructure.

Mortgage and Real Estate Financing

The mortgage industry benefits from holistic underwriting that looks beyond debt-to-income ratios and credit scores. By analyzing rental payment history, savings patterns, and income stability through transaction data, lenders can approve qualified borrowers who might decline under traditional models. This is especially valuable for self-employed individuals, freelancers, and those with non-traditional income sources who demonstrate financial responsibility through alternative means.

Conclusion

The future of lending unequivocally belongs to Unified Financial Intelligence. By harnessing AI-driven lending solutions, alternative data, and holistic underwriting, financial institutions can elevate credit decision-making to new heights, delivering smarter, faster, and more inclusive loan approvals. This shift not only optimizes risk management but also drives financial inclusion on a global scale.

Discover how Fintly empowers lenders with unified financial insights and AI-driven credit decisioning for next-generation lending excellence. Book a demo today and transform your lending operations with cutting-edge technology.

Author

Subject Matter Experts (Lending) Fintly.co

Vijay Mali is a results-driven professional with deep expertise in HFC/NBFC startups, compliance, and underwriting. He specializes in delivering end-to-end solutions for financial institutions, focusing on Business Rule Engines (BRE), workflow automation, and AI-driven credit decision-making. He is passionate about leveraging Machine Learning (ML) scorecards and AI-powered risk assessment to optimize lending processes and drive digital transformation in the financial sector.