In 2023, the global economy bled an estimated $485.6 billion due to financial fraud. That is a massive transfer of wealth from legitimate businesses to bad actors. If you operate in finance or fintech, the question has shifted from whether you will be a victim to if you can spot the attack at the first glance through effective fraud analysis techniques.

So, what is the defense? At its core, fraud analysis is the systematic process of gathering and analyzing financial data to detect anomalies, patterns, and hidden behaviors that indicate fraudulent activity. This guide breaks down exactly how modern fraud analysis works. You will learn the core concepts, the analytical techniques financial institutions use to catch anomalies, and how advanced fraud analysis techniques help build a prevention framework that stops revenue leakage before it happens.

Fraud Analysis Basics: Decoding the Core Concepts

Before you can stop fraud, you have to understand how it hides in plain sight. Fraud analysis isn’t just about looking for stolen credit cards; it is about understanding behavioral deviations through proven fraud analysis techniques.

When a user interacts with a financial system, they leave a digital footprint. Fraud risk assessment involves establishing a baseline of “normal” behavior for that footprint. If a customer who usually logs in from Pune to buy groceries suddenly attempts a $5,000 wire transfer from an IP address in Eastern Europe, the system flags it.

To dig deeper into these baseline behaviors, reading up on the broader fraud detection and prevention in the fintech ecosystem can help you map out exactly where your industry-specific vulnerabilities lie and which fraud analysis techniques are most effective.

The Anatomy of a Transaction Evaluation

A solid fraud analysis looks at three critical variables during every interaction using data-driven fraud analysis techniques:

- Velocity: How fast are transactions happening? (e.g., five rapid-fire transactions in one minute).

- Location & Device: Does the device location match the billing address? Is the device recognized?

- Value: Is the transaction amount drastically outside the user’s historical spending habits?

Modern Analysis Techniques: How Financial Institutions Spot Fraud

Fraudsters no longer operate manually. They use automated bots, synthetic identities, and machine learning to bypass basic security. To keep up, fraud analysis tools have evolved from static frameworks to dynamic intelligence powered by modern fraud analysis techniques.

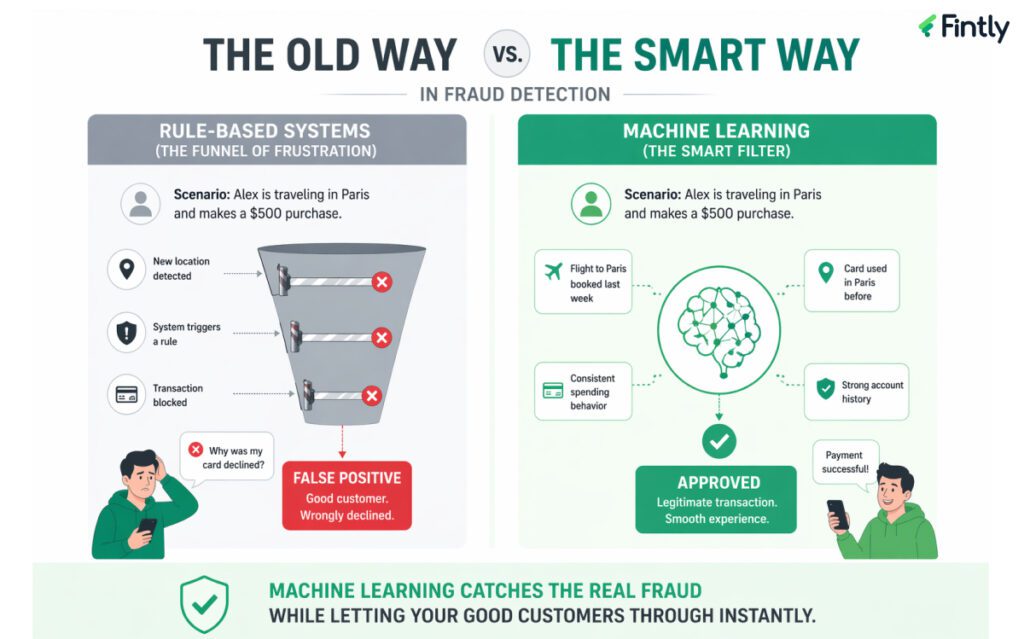

Rule-Based Systems vs. Machine Learning

For decades, banks relied heavily on rule-based systems. These systems operate strict “if-then” logic. (For example, if the transaction is over $10,000, then flag it for manual review).

The problem? Rule-based systems are rigid. They generate massive amounts of false positives, flagging legitimate customers, and causing friction at checkout. Today, modern risk platforms leverage AI and machine learning to analyze thousands of data points in milliseconds , making these fraud analysis techniques significantly more accurate and scalable.

| Feature | Rule-Based Fraud Detection | Machine Learning Fraud Detection |

| Underlying Logic | Static “If-Then” rules | Dynamic pattern recognition |

| Adaptability | Requires manual, human updates | Learns from new data automatically |

| False Positives | High (creates customer friction) | Low (precision improves over time) |

| Scalability | Hard to scale across diverse datasets | Highly scalable across complex data streams |

If you want to explore the specific software side of this shift, check out our guide on fraud detection techniques and tools.

The Cost of Ignoring the Data

You cannot manage what you do not measure. Fraud prevention requires understanding the scale of the threat and the technology gap in the market through reliable fraud analysis techniques:

- According to a Nasdaq Verafin report, global losses tied to fraud reached approximately $485.6 billion in 2023. This means fraud is a macroeconomic threat, and your prevention strategy is directly tied to your company’s bottom line and survival.

- Despite the rise in sophisticated attacks, research published in 2025 indicates that only 22% of businesses actively utilized artificial intelligence in their fraud detection workflows as of 2023. This highlights a massive technological gap, making companies that rely purely on legacy systems the easiest targets for automated fraud networks despite advancements in fraud analysis techniques.

Real-World Case Study: Catching Synthetic Identity Fraud

Theoretical frameworks only go so far. Let’s look at how advanced fraud analysis operates in the wild.

In early 2024, fraud rings heavily deployed “synthetic identities”, fake personas created by stitching together real and fabricated information (like a real Social Security Number matched with a fake name). Because the data looks real on paper, traditional identity checks often fail to spot them.

The OmniGraph Approach: PayPal utilized an internal system called OmniGraph to combat this specific threat. Instead of looking at transactions in isolation, OmniGraph mapped cross-platform behavior graphs. By linking user activity across banking, e-commerce, and social channels, the system looked for unnatural connections between accounts. In just the first quarter of 2024, this relational data analysis successfully identified and blocked $120 million in synthetic identity fraud.

This proves that analyzing relationships between data points is far more effective than analyzing isolated events, , especially when supported by intelligent fraud analysis techniques.

The Fraud Prevention Framework: Proactive Risk Management

Detecting fraud is reactive; preventing it is proactive. A comprehensive fraud risk management framework requires layering different defenses so that if one fails, another catches the anomaly.

1. Identity Verification (KYC): Stop bad actors at the door. Use biometrics, liveness checks, and document verification during the initial onboarding phase.

2. Continuous Monitoring: Fraud analysis doesn’t stop after a successful login. You must monitor session behavior, device intelligence, and transaction velocity continuously using real-time fraud analysis techniques.

3. Automated Intervention: When a threat is detected, the system should automatically step up authentication (like requiring an OTP) or freeze the transaction without waiting for a human analyst.

Integrating specialized tools makes this layered approach seamless. Fintly is designed to help financial teams spot anomalies before the damage is done. By implementing our Early Warning Signs architecture, your team can identify deteriorating credit profiles or fraudulent transaction patterns automatically, allowing you to act swiftly and decisively.

Conclusion

Fraud analysis is the engine that powers secure financial ecosystems. Moving away from static, rule-based systems toward dynamic, data-driven analysis is a baseline requirement. By understanding the core concepts, adopting effective fraud analysis techniques, and implementing a layered prevention framework, you protect your revenue, maintain compliance, and build trust with your users.

If you are ready to upgrade your fraud risk management and stop relying on outdated detection methods, it is time to talk to the experts. Contact Us today to see how Fintly can secure your operations.

Author

Subject Matter Experts (Lending) Fintly.co

Vijay Mali is a results-driven professional with deep expertise in HFC/NBFC startups, compliance, and underwriting. He specializes in delivering end-to-end solutions for financial institutions, focusing on Business Rule Engines (BRE), workflow automation, and AI-driven credit decision-making. He is passionate about leveraging Machine Learning (ML) scorecards and AI-powered risk assessment to optimize lending processes and drive digital transformation in the financial sector.